Starting to be effective on January 1st, 2024, the new law known as the Corporate Transparency Act requires certain companies to disclose private information to the Financial Crimes Enforcement Network (FinCEN).

As a component of the Anti-Money Laundering Act of 2020, the CTA was imposed by Congress to regulate shell companies and prevent money laundering, terrorist financing, human trafficking, and securities fraud.

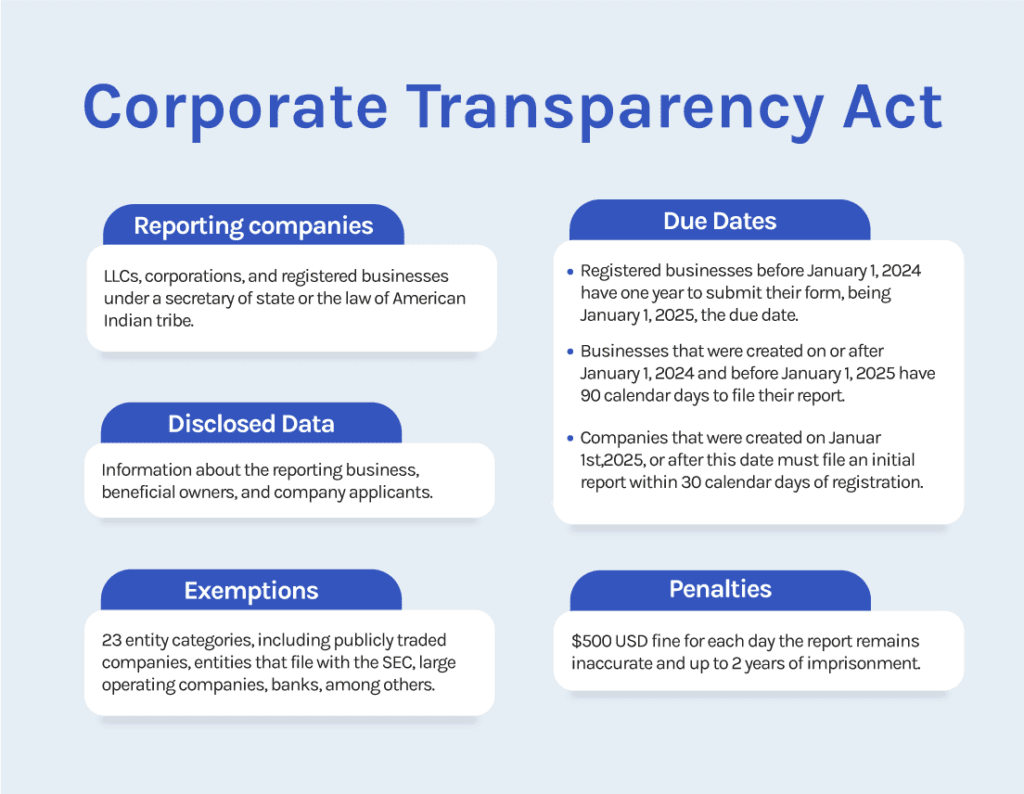

The Corporate Transparency Act affects small businesses by requiring corporations, LLCs, or other entities created under the law of state to file a beneficial ownership information (BOI) report. In compliance with The Final Rule, businesses have to provide information about the reporting company, its beneficial owners, and company applicants. FinCEN estimates that 32 million businesses in the US will be subject to these reporting rules.

There are some exemptions to the CTA, and specific data that must be disclosed by small businesses, which we will discuss in the article.

Key takeaways

Taking effect on January 1, 2024, the Corporate Transparency Act requires businesses to file a BOI report with the Financial Crimes Enforcement Network (FinCEN), a division of the U.S. Department of Treasury. This report will include information about the reporting company, its beneficial owners, and business applicants.

the final rule: What are the CTA requirements?

The final rule is a law that implements the Corporate Transparency Act. which was issued by the Financial Crimes Enforcement Network (FinCEN) on September 28, 2020.

In compliance with the final rule, certain corporations and limited liability companies (LLCs) must report information about their beneficial owners to FinCEN. Reporting companies are required to provide the full legal name, date of birth, address, and unique identification number of each beneficial owner who directly or indirectly owns 25% or more of the reporting company’s equity interests, and one individual who has significant managerial control over the reporting company. The final rule aims to enhance the transparency of corporate ownership and prevent the use of anonymous shell companies for illicit purposes.

Who is required to report to the FinCEN?

The Corporate Transparency Act requires the following entities and individuals to report specific data:

Reporting companies

Reporting companies are divided into two: Domestic reporting companies and foreign reporting companies, which are defined below.

![]() Domestic reporting companies

Domestic reporting companies

Any entity that is

- A corporation

- A limited liability company (LLC), limited liability partnership (LLP), a business trust, or any business entity created under a secretary of state or any similar office under the law of a state or American Indian tribe.

![]() Foreign reporting company

Foreign reporting company

Any entity that is

- A corporation

- A limited liability company (LLC), limited liability partnership (LLP), or business trust or

- Formed under the law of a foreign country and registered to do business in the United States by the filing of a document with a secretary of state or any similar office under the law of a state or American Indian tribe.

Beneficial owners

As defined by the Final Rule, a beneficial owner includes any individual who exercises “substantial control” over the reporting company and owns or controls at least 25% ownership interests of the business.

A reporting company will always have at least one owner with substantial control and possibly several owners with such control, even if no individual reaches a 25% ownership interest.

Individuals who are considered to exercise substantial control are those who:

![]() Serve as a senior office for the reporting company, such as CEOs, CFOs, COOs, and general counsel.

Serve as a senior office for the reporting company, such as CEOs, CFOs, COOs, and general counsel.![]() Have authority over the appointment or removal of any senior officer or a majority of the board of directors

Have authority over the appointment or removal of any senior officer or a majority of the board of directors![]() Have authority to direct or determine important decisions made by the reporting company, such as those related to the sale or transfer of the business’s assets, major expenditures or investments, and merger or dissolution of the reporting company, among others.

Have authority to direct or determine important decisions made by the reporting company, such as those related to the sale or transfer of the business’s assets, major expenditures or investments, and merger or dissolution of the reporting company, among others.

Under the CTA, ownership interest is determined by a variety of factors:

![]() The 25% threshold is met taking into account stock and other interests, capital interests, profit interests, put, call, and straddles.

The 25% threshold is met taking into account stock and other interests, capital interests, profit interests, put, call, and straddles.

![]() For Reporting Companies that issue shares of stock, the threshold is measured as a percentage of the greater of either the total voting power of all ownership interests entitled to vote or the total outstanding value of all classes of ownership interests.

For Reporting Companies that issue shares of stock, the threshold is measured as a percentage of the greater of either the total voting power of all ownership interests entitled to vote or the total outstanding value of all classes of ownership interests.

There are exemptions for those who are considered beneficial owners:

![]() Minor children (however, the parent’s or legal guardian’s information of the child must be provided)

Minor children (however, the parent’s or legal guardian’s information of the child must be provided)![]() Nominees, intermediaries, custodians, or agents on behalf of other individuals

Nominees, intermediaries, custodians, or agents on behalf of other individuals![]() Employees who are not senior officers of the entity and whose substantial control derives solely from their employment status

Employees who are not senior officers of the entity and whose substantial control derives solely from their employment status![]() Individuals whose only interest is a future interest through a right of inheritance

Individuals whose only interest is a future interest through a right of inheritance![]() Creditors

Creditors

Company applicants

According to The Final Rule, a company applicant is the individual who directly files the document to create or register the reporting company, and who is responsible for directing or controlling such filing. There can be more than one Company Applicant.

Required information

Reporting Company

![]() The business will have to provide the following identification data about itself:

The business will have to provide the following identification data about itself:![]() Full legal name

Full legal name![]() Trade name, or Doing Business As (DBA) name

Trade name, or Doing Business As (DBA) name![]() Current address, principal place of business, or primary location

Current address, principal place of business, or primary location![]() Jurisdiction in which it was formed or first registered

Jurisdiction in which it was formed or first registered![]() IRS Tax identification number

IRS Tax identification number

Business owners and company applicants

![]() Legal name

Legal name![]() Date of birth

Date of birth![]() Current Home Address

Current Home Address![]() ID Number and issuing jurisdiction (passport, driver’s license, etc.)

ID Number and issuing jurisdiction (passport, driver’s license, etc.)![]() Image of the document with ID

Image of the document with ID

After an initial filing, reporting companies have 30 days to file an updated report after any change concerning information previously reported.

When should you file the CTA report?

The dates for filing differ for existing companies and newly created ones.

![]() Existing companies: Reporting companies that were created or registered before January 1, 2024, must file their initial BOI reports one year after the CTA is effective, for existing companies must report not later than January 1, 2025.

Existing companies: Reporting companies that were created or registered before January 1, 2024, must file their initial BOI reports one year after the CTA is effective, for existing companies must report not later than January 1, 2025.

![]() New companies: Reporting companies created or registered to do business on or after January 1, 2024, the initial report is due 30 calendar days from the date on which it receives notice of its effective creation.

New companies: Reporting companies created or registered to do business on or after January 1, 2024, the initial report is due 30 calendar days from the date on which it receives notice of its effective creation.

If there are any corrections or changes of ownership, a new report must be filed within 30 days of the correction or change. These changes may include a change of address, a change in senior management, the death of an owner, or a business interest pass on to new beneficiaries. After filing the report and making the needed modifications, there are no ongoing filing requirements.

Exemptions

The CTA identifies 23 entity types that are not regarded as reporting companies. Most exemptions are for entities that are already subject to substantial federal or state regulation. Exemptions include publicly traded companies and other entities that file reports with the SEC, such as the ones mentioned below:

-

- Large operating companies: Entities that employ more than 20 employees on a full-time basis in the US, have filed a federal US income tax return for the year prior showing more than $5 million in gross receipts or sales, and operate from physical office premises in the US.

- Securities issuers

- Domestic governmental authorities

- Banks

- Domestic credit unions

- Depository institution-holding companies

- Money transmitting businesses

- Brokers or dealers in securities

- Securities exchange or clearing agencies

- Other Exchange Act registered agencies

- Registered investment companies and advisers

- Venture capital fund advisers

- Insurance companies

- State-licensed insurance producers

- Entities registered under the Commodity Exchange Act

- Accounting firms

- Public utilities

- Financial market utilities

- Pooled investment vehicles

- Tax-exempt entities

- Entities assisting tax-exempt entities,

- Subsidiaries of certain exempt entities

- Inactive businesses.

Penalties

Not complying with the Corporate Transparency Act may lead to several penalties.

Failure to comply, fraudulent reports, or unauthorized disclosure of BOI can result in civil or criminal actions, as described below:

Not filing or updating a report: This may result in civil fines of $500 each day the report remains inaccurate Also, the violator may be subject to criminal penalties of a $10,000 fine or imprisonment for up to 2 years.

Disclosing a report: Revealing sensitive information without authorization may implicate a $500 penalty per day (up to $250,000) and up to 5 years in jail.

Who will have access to my personal and business information?

The reports filed with FinCEN will not be accessible to the public and are not subject to requests under the Freedom of Information Act. This information will be subject to strict use and security protocols.

The provided information will only be accessible to the following agencies:

![]() Federal agencies engaged in national security, intelligence, and civil and criminal law enforcement.

Federal agencies engaged in national security, intelligence, and civil and criminal law enforcement.![]() State and local law enforcement agencies with a court order.

State and local law enforcement agencies with a court order.![]() The Department of Treasury

The Department of Treasury![]() Financial institutions that assist FinCEN in their anti-money laundering compliance activities

Financial institutions that assist FinCEN in their anti-money laundering compliance activities![]() Government regulators of financial institutions

Government regulators of financial institutions

How to file my Corporate Transparency Act report

As a small business owner, the first step is to determine whether your company is required to file its report. A business attorney and tax advisor can assist with this process and help you evaluate a compliance plan to:

- Determine if your business falls under a CTA reporting company

- Identify beneficial owners and company applicants

- Keep the information updated and avoid penalties

The corporate lawyer will need to revise your business’s structure and operating agreements to confirm the company’s eligibility and assist in the process of gathering the information, updating internal policies to effectively report it, and creating a tracking system to ensure the data remains updated.

To file the BOI report, you will need to submit a form electronically with FinCEN through a system that is going to be available on the institution’s website from January 1, 2024. FinCEN will not start accepting CTA reports prior to this date. There is no fee for filing the reports

Although more businesses are more than a year away from meeting the deadline, the best practice is to seek legal and tax guidance to prepare for complying with the Corporate Transparency Act and start gathering the corresponding data.

How can corporate attorneys from Motiva Business Law help?

Our business attorneys will review your corporate documents and determine whether your business needs to file a BOI report. We help you stay up-to-date with the CTA and comply with the regulations of your industry.

Our lawyers will help you protect your business. Call at 630 (517) 5529 and schedule a consultation.